In the first 8 months of the year, there was a blizzard of announcements around housing, land for housing and construction costs. Government proposals include:

- requiring tier 1 and 2 councils to live-zone feasible development capacity to provide for at least 30 years of housing demand

- requiring cities to be allowed to expand outwards at the urban fringe

- strengthening intensification provisions in the National Policy Statement on Urban Development, allowing greater density around strategic transport corridors

- allowing self-contained, single-storey detached houses of up to 60 m² – granny flats – that meet certain requirements to be built without a building or resource consent

- making it easier to use certain building products from overseas, with building consent authorities required to accept recognised overseas products as compliant with the New Zealand Building Code

- making building consent variations easier

- making remote building inspections the default approach, reducing delays and costs.

While some changes will just affect new home construction, others are likely to encourage more privately held land to be made available for development. ‘With the requirement for councils to zone land for 30 years of housing supply, people who remain holding land and not doing anything with it will miss the boat,’ says Matthew Curtis, Senior Research Analyst at BRANZ.

Implementing the changes will in most cases require amendments to the Building Act or Resource Management Act or

regulations, so any new rules won’t come into effect for a while.

housing stock than many other countries (Source: OECD Affordable Housing Database).

Why the changes?

We don’t have enough homes. For each 1,000 inhabitants, we have 396 dwellings. That’s fewer than the OECD average of 468 and well below the EU average of 514. For almost the entire 3 decades from 1990 to 2020, we had fewer homes for our population size than Australia, Canada, the UK or the US.

The tide has turned, however. While there remains a shortage of housing, the position isn’t as dire as it was 2-3 years ago.

‘In 2020/2021, interest rates were so low that they eventually pushed annual dwelling consents over 51,000,’ Hamish Fitchett, Senior Economic Analyst at the Reserve Bank, told Build.

He points to OECD data that shows that Aotearoa New Zealand has very recently been one of the leaders in the number of new dwellings it is building as a percentage of total housing stock (Figure 1). By this measure, we have been building around double the number of dwellings that we were in 2011 and building more than most comparable countries.

While it takes a long time to make a difference, and new consent numbers have slowed significantly from the peak of 2 years ago, there are some reasons for optimism. There is general agreement – and relief – that the worst point of this cycle is largely over.

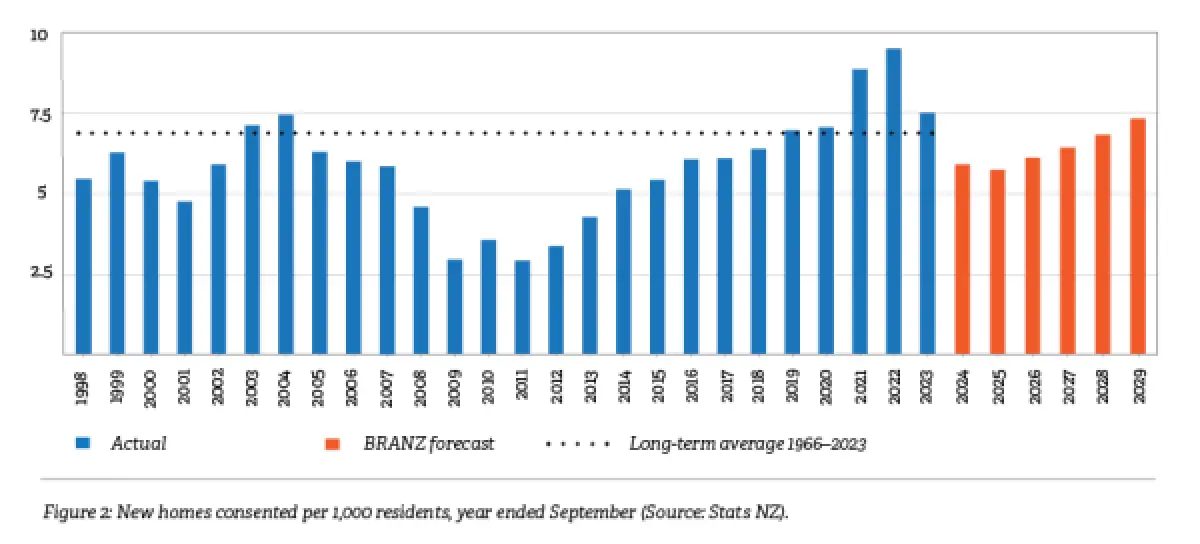

‘We could be close to the low point,’ Reserve Bank Economic Advisor John Knowles told Build. ‘Although consents have fallen in response to higher interest rates, it is encouraging that they haven’t fallen more. They are not very low by historic comparison, even with higher interest rates. Things were much worse in the global financial crisis’’. (As Figure 2 shows, in the year to September 2011, there were just 3.1 dwellings consented per 1,000 residents – less than half the figures achieved more recently.)

‘A bit of perspective is handy,’ CoreLogic’s Chief Property Economist Kelvin Davidson told Build. ‘The numbers of new homes we are building are still good historically.’

The average annual number of homes consented per 1,000 residents between 1966 and 2023 was 6.7. In the 12 months to mid-2024, as the house building industry approached a trough, the number stood at 6.6 – very close to the long-run average (see Figure 2).

There are reasons for optimism for the construction sector in the longer-term. Some forecasts see dwelling consent numbers reaching the bottom of a trough with around 30,000 consents per year in early 2025, growing to approximately 40,000 consents per year by the end of the decade. These forecasts mostly account for the government announcements in the first half of the year.

No return to 51,000 consents per year

A return to the record highs of recent years is not on the cards even with the government’s recent initiatives. ‘Even by 2030, we are not likely to return to the 51,000 annual consents we saw mid-2022,’ says Matthew Curtis, ‘But 40,000 consents a year is still a good number.’

One thing to bear in mind is that the figures don’t take account of demolitions/deconstructions, so they slightly overstate actual growth. For example, if one old house is taken down and replaced by four townhouses, the consents for the townhouses are recorded but the demolition usually isn’t. The data says there are four new homes, where in fact the net gain is only three.

Does the push to free up land ensure more homes?

Rezoning or upzoning significant areas of land to make it available for housing, as the government is promoting, generally leads to more homes being built.

Whether or not that happens in any given location depends largely on the infrastructure in place to support the housing. One property developer told the Waikato Times in July, ‘I have a number of sites in Hamilton that I can’t develop because there’s no sewer infrastructure.’

Infrastructure capacity limits or poor performance are causing problems for towns and cities large and small.

In July, the South Wairarapa District Council announced that it would be pausing new wastewater connections in Greytown because it couldn’t handle the requirements of a large residential development proposal.

The previous August, it had paused all applications for new wastewater connections in Martinborough. New wastewater connections have also been delayed in Warkworth and other centres.

Local Government New Zealand President Sam Broughton says, ‘The logjam on housing has happened because councils are not resourced to support the level of growth that everyone knows we need … New housing requires roads, footpaths, green space and services, which are currently really expensive for councils and ratepayers.’

How these are funded is the key issue. ‘A 50% share of the GST revenue on new builds – as signalled in the Coalition Agreement – is a good place to start,’ Sam Broughton says. ‘Rates alone simply can’t cut it.’

The government has said it is working on city and regional deals – agreements with individual councils about projects and their funding. Options such as sharing the GST earned on houses built are being considered.

The point that local body rates can’t be increased to fund the growth required is widely accepted. ‘There have been signals that growth needs to pay for growth,’ says Matthew Curtis. ‘This means targeted rates or increased development contributions for new development.’ While targeted rates are not in wide use, they do exist in a few areas.

Little risk of changes being undone

‘Freeing up more land doesn’t automatically mean that it will be built on,’ Kelvin Davidson says, ‘and it takes time for the flow of new dwellings to come through.’

But there is an optimism that policy changes freeing up land will have a positive impact on housing supply and that there may be comparatively little political risk around it.

While it isn’t uncommon for the actions of one government to be undone by a subsequent government with a different ideology, that may be less likely to happen with some recent initiatives. ‘There is a growing consensus in the economics community that allowing greater supply is the most effective way to improve housing affordability,’ John Knowles told Build.

Airbnbs and holiday homes not the problem

Occasionally, you hear the suggestion that the housing shortage is the result of far too many homes left empty or only occasionally occupied, but internationally, we rate very low on that score.

OECD figures show that just 6% of our dwelling stock is made up of vacant dwellings or holiday homes, compared to 9.6% in Australia and higher figures in many other countries.