Resilience can be measured in several ways. Levy-funded research looked at the financial ratios of different-sized residential building firms to see if their resilience has improved over time. The answer is yes for large and medium-sized builders, but concern remains for smaller building firms.

Large builders increase their share

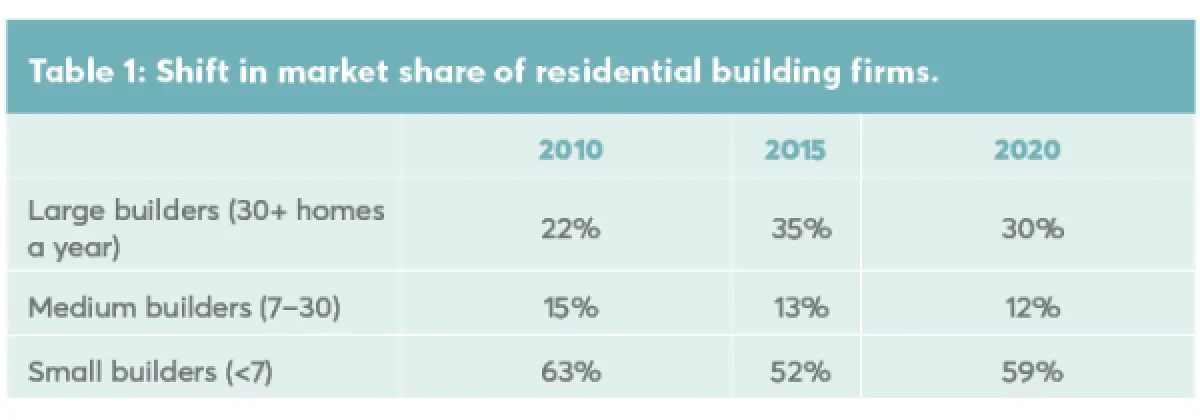

Large builders – those constructing more than 30 dwellings a year – are completing a greater share of Aotearoa New Zealand’s residential buildings – up from 22% in 2010 to 30% in 2020. This has been driven by the continued rise of national franchise builders and transportable home manufacturers.

Growth in homes built by large builders meant that the smaller builders were doing less when comparing 2010 to 2020. Small building firms were doing 59% of new residential dwellings in 2020 compared to 63% in 2010. However, in 2015, their share had dropped to 52%, so 59% represents a bounce back for them (see Table 1).

Medium-sized builders – those building 7–30 homes a year – slowly lost market share over the decade, down from 15% of new residential dwellings in 2010 to 12% in 2020.

What might be a surprise is that large builders make up 1% of all residential building firms in Aotearoa and that has stayed pretty much the same over the last decade. There are more medium-sized firms now – 7% of firms, up from 3% in 2010. Together, the large and medium-sized firms are 8% of all residential building firms but account for 42% of Aotearoa’s new houses. Scale definitely matters.

A glimpse at the financials

Looking at some of the financial data, there are quite different business models in play for the large and medium-sized firms compared to the small operators.

Smaller firms tend to have very few employees and do most of the work themselves – they don’t spend a lot on subcontractors. Only 3% of small building firms have six or more employees, and less than 10% of small builders spend 50% or more of their expenses on subcontractors.

This switches around for medium and large building firms. Over 50% of medium builders and 70% of large builders have six or more employees. Medium and large builders spend more on subcontractors – 45% of medium builders spend 50% or more of their expenses on subcontractors, and this increases to 60% for large builders.

The number of employees has not changed much between 2010 and 2020 for any of the size bands. The percentage of small building firms spending 50% or more of their expenses on subcontractors has also stayed pretty much the same over this time.

The percentage of medium-sized building firms spending 50% or more of their expenses on subcontractors steadily decreased between 2010 and 2020 – down from 60% to 45%. There was a smaller reduction for large building firms – from 67% to 60% – although it jumped up to 83% in 2015.

Is everyone improving?

A median or average is sometimes reported as a measure of the financial health of building and construction firms in Aotearoa. This can give a good overall picture but doesn’t reveal the spread – how the worst and best firms are doing. To do this, we asked Stats NZ to provide maximum and minimum figures for financial ratios.

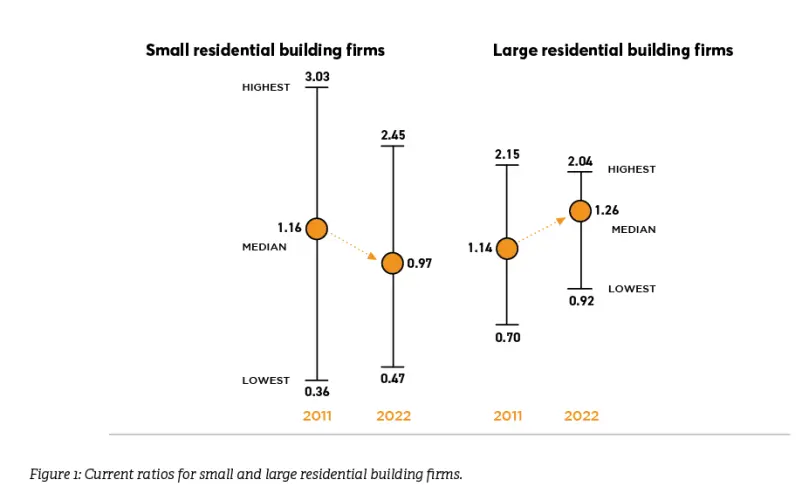

A good example is the improvement in current ratio by large residential building firms. Current ratio gives insight into a firm’s ability to pay its short-term liabilities. Anything under 1 suggests difficulty.

Figure 1 shows that between 2011 and 2022, the median for large firms increased from 1.14 to 1.26, telling us that, overall, their ability to pay has improved. What is even better is the lowest value went up – from 0.7 to 0.92 – so even the worst-performing large firm is almost at a healthy level. The median for medium-sized firms went down very slightly, but the worst-performing medium firms saw a similar improvement to that of large firms.

Unfortunately, small residential building firms have not shown the same improvement. The median dropped from 1.16 to 0.97 between 2011 and 2022. Most of that drop occurred early on, with a slow recovery towards the end. There is a glimmer of good news with the poorest-performing small firms improving their current ratios from 0.36 to 0.47, but this is still a long way below the ideal of 1.

It is a similar story for other financial ratios such as liability structure and return on assets. Large residential building firms have improved their ratios, while small and medium-sized firms have either stagnated or struggled to improve their financial strength.

What does this mean for resilience of the sector?

The improvement in financial ratios for large residential building firms and the fact that they are undertaking a higher percentage of Aotearoa’s new builds indicate improvement in resilience. This is especially the case when even the bottom end of this grouping has improved under these ratios. It isn’t just a case of the best large firms dragging the performance of everyone else up.

The not-so-good news is that small builders have not experienced similar financial improvements over the last decade. Small builders still account for nearly 60% of new homes built in Aotearoa, so the lack of improvement remains a concern for overall industry resilience.

The question is whether efforts to improve resilience should go towards lifting up the performance of the many small firms, or do we try and grow the share of large and medium-sized firms who already demonstrate better performance?